Last updated: April 2026

TL;DR: Home insurance premiums are up 46 percent since 2021, with Florida homeowners now averaging $10,996 a year — the highest in the country. The primary driver is zip-code-level climate risk repricing by insurers, not individual homeowner claims history. Check your replacement cost coverage and adjust your deductible before your next renewal.

Last updated: May 2026

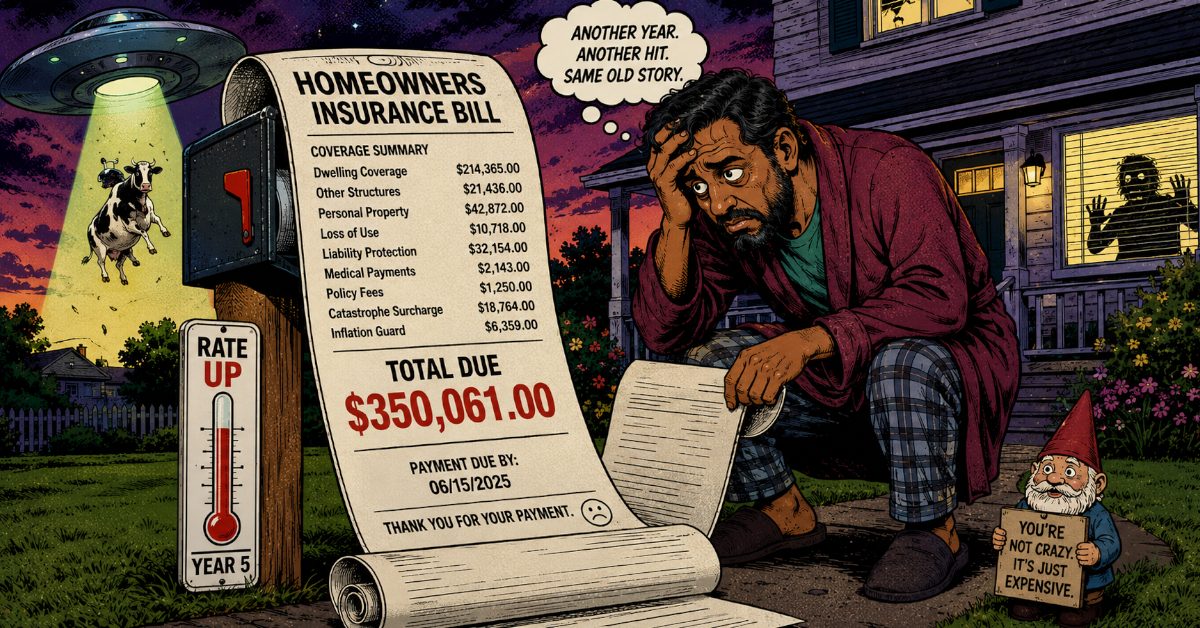

Florida homeowners now pay an average of $10,996 a year for home insurance, according to Florida Department of Insurance 2026 data. That is not a typo. That is a mortgage payment in some states. Your premium did not go up because your house got riskier. It went up because insurers are repricing climate risk across entire zip codes at once.

Nationally, home insurance premiums are up 46 percent since 2021, nearly three times the rate of general inflation over the same period, according to Insurance Information Institute 2026 data. This is the fifth consecutive year of increases. One in three homeowners says they are not confident they can maintain their current coverage through 2026, per an NPR home insurance investigation published May 2026.

The mechanism is not complicated. Insurers lost money in catastrophic loss years, reinsurers raised their rates, and those costs passed straight to you. When a single hurricane season wipes out reserves built over a decade, the math resets for every policyholder in the region, regardless of whether your house was touched. Your zip code is now your risk rating more than your claims history.

The state-level spread is wide. Louisiana averages roughly $5,400 annually. Oklahoma sits near $5,200. Texas averages around $4,400. Move to the Midwest and the number drops fast: Ohio homeowners average closer to $1,400 a year, and Wisconsin runs even lower. The gap between Florida and Ohio is nearly $9,600 per year for identical coverage structures. That difference is entirely climate exposure and carrier withdrawal from high-risk markets.

If you are in Florida, Louisiana, or coastal Texas, your options have narrowed. Several major carriers have exited those markets entirely. What remains is state-backed insurers of last resort and a shrinking pool of private options. Check your current policy’s replacement cost coverage. Many homeowners discover mid-claim that their coverage caps were set years ago and no longer reflect actual rebuild costs, which have risen 30 to 40 percent since 2020 per Insurance Information Institute reporting.

You can use the Ohio home renovation cost calculator to cross-check your current coverage against realistic rebuild costs in your area before your next renewal hits.

If you are outside the highest-risk states, raise your deductible from $1,000 to $2,500. The premium savings typically run $300 to $600 a year, according to Insurance Information Institute guidance. That is real money back in your pocket with minimal exposure increase if you have a cash reserve.

Premium increases are not stopping in 2026. Reinsurance contracts are repriced annually, and climate loss data keeps moving in one direction. Get your replacement cost number right, check your deductible, and do not wait until your renewal notice arrives to find out what you are actually paying for.

Vanderflip Home has a free renovation cost calculator that shows current rebuild costs by state so you can compare them against your existing coverage limits.

FREQUENTLY ASKED QUESTIONS

What is the average home insurance cost by state in 2026?

Costs range widely: Florida averages $10,996 per year, Louisiana roughly $5,400, Texas around $4,400, and Ohio closer to $1,400, according to Insurance Information Institute 2026 data. Your state’s climate exposure and carrier availability are the primary drivers.

Why did my home insurance go up so much this year?

Insurers are repricing climate risk across entire zip codes, not based on your individual claims history. Reinsurance costs have risen sharply after major catastrophic loss years, and those increases pass directly to policyholders — whether your home was affected or not.

What can I do to lower my home insurance premium in 2026?

Raising your deductible from $1,000 to $2,500 typically saves $300 to $600 per year in lower-risk states, per Insurance Information Institute guidance. Also verify your replacement cost coverage reflects current rebuild costs, which have risen 30 to 40 percent since 2020.